LIC || LIC latest news || Sub: LIC IPO: A big test for India

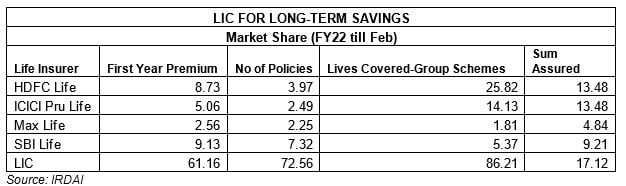

Did you know that Life Insurance Corporation of India (LIC) was an amalgam of 245 entities, including 154 life insurers? They were bound together by an act of parliament in September 1956, after some private insurers were found to be committing fraud. Today, over 20 years since the private sector has entered the fray, LIC still commands a 61 percent share of the new premium collected and over 72.5 percent of the policies sold in the country.

That’s not all. LIC’s assets i.e. Rs 39.7 trillion, exceeds the GDP of several economies. Additionally, its assets are 1.1 times more than the entire Indian MF industry i.e. Rs 31.4 trillion (till March 31, 2021). It also equals nearly 19 percent of India’s GDP. And its equity investments, a small share of AUM, accounts for 4 percent of the total market capitalization of all stocks listed on the NSE.

Clearly, when it comes to size and scale, it doesn’t get bigger than LIC. And that perhaps is where the challenge lies. The IPO is bound to set records in terms of size, retail subscription et al, but can it sail through without any hiccups? That remains the big question.

CHALLENGES OF A MEGA IPO

The LIC IPO, no matter what valuation metric or parameter you use will clearly be the largest in Indian history. Most estimates, even the widest, would put the range between Rs 30,000 to Rs 60,000 crore. That’s more than twice the size of Paytm (Rs 18,300 crore) or Coal India (Rs 15,200 crore) IPOs. Mopping up such a large sum is bound to be a tall task. This, especially since the proportion reserved for resident individuals of 35 percent, would alone be almost the size of India’s earlier mega IPOs.

India at the end of January 2022 had a total of 8.4 crore active demat accounts. And it would take anywhere from a minimum of about 7.5 lakh (if each invests Rs 2 lakh) to over 2 crore investors to see the offer through. To put this in context, Paytm has 10.4 lakh shareholders who invested up to Rs 2 lakh. The number for Zomato is 7.9 lakh. So we are talking of a big leap for LIC.

Can LIC build up the frenzy to get a wide swathe of investors to subscribe? That remains the big question. It must be noted, that LIC has reserved 10 percent of its IPO for its 29 crore policyholders and 5 percentfor its employees. The insurer's policyholder base is huge and it has been trying to get them to open demat accounts and subscribe to the offer with the lure of a discount, but from what we learn, its vast agency force hasn’t been mobilized yet to drive subscriptions. That can be a critical factor in the success of its offer.

The other hurdle for LIC is that this isn’t the best time to tap foreign money, given that foreign portfolio investors have been pulling out funds from several emerging markets, including India, ahead of a likely US Federal Reserve action to up rates and tighten liquidity. This has also hurt the general market sentiment.

Besides, the life insurance business isn’t one that’s easy to understand and retail investors would find it difficult to assess its performance and valuation. Then, there’s also the business itself. While there are the positives of scale and dominance, there are also some concerns and triggers to weigh. Let’s take a quick look at some of these.

THE PROS AND CONS FOR LIC

What LIC clearly has going for it, is its scale, dominant market share and the huge trust that Indians have in the brand. In case you didn’t know, LIC is the No. 2 brand in the country after Tata. And that’s a big plus.

What’s not really so comforting is the current nature of its business and some operating metrics, for which its market share provides some insights. While it sells 72.5 percent of the policies in the country, its value share is 61 percent and its share of protection in individual policies is low, which results in just a 17 percent share of the total sum assured. This makes LIC more a seller of savings products than a life insurance provider, and limits its profitability—its margins are about half of the industry peers.

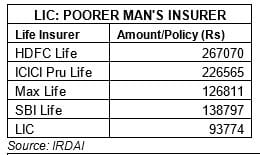

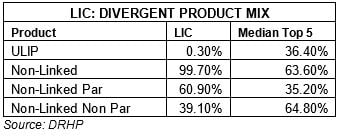

The nature of products it sells, more participating policies and limited ULIPs also impact its value share resulting in its per policy value being far lower than peers at sub Rs 1 lakh versus nearly Rs 2.7 lakh for HDFC Life Insurance and Rs 2.3 lakh for ICICI Prudential Life Insurance. This also impacts employee productivity. LIC’s revenue per employee is about Rs 2.5 lakh compared to the median of the top 5 private insurers at near Rs 11 lakh.

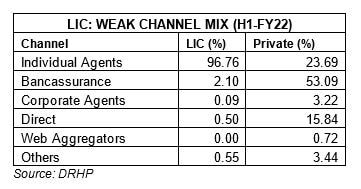

Its marketing efforts are also skewed with an over-dependence on its strong agency network, which no doubt is an asset but leads to high commission payouts. Besides, there is little diversification and very little low-cost direct or online distribution. The latter became evident during Covid when its business was impacted far more than its private peers due to the lockdown.

The other niggling points of concern are how LIC might use its resources and whether it will act in the interests of the minority shareholders. It infused Rs 4,743 crore into IDBI Bank using policyholders’ funds, and such other transactions to salvage situations where the government may require support are quite possible. In fact, the insurer is quite candid in its risk factors, stating that: “Our Corporation may be required to take certain actions in furtherance of the GoI’s economic or policy objectives. There can be no assurance that such actions would necessarily be beneficial to our Corporation. "The interests of the promoter as the controlling shareholder of our Corporation could be in conflict with the interests of our other shareholders. We cannot assure you that the promoter will act to resolve any conflicts of interest in favour of our corporation or the other shareholders. To the extent that the interests of the Promoter differ from your interests, you may be disadvantaged by any action that the Promoter may seek to pursue,” LIC said last week.

In a nutshell, therefore, LIC has scale, but also operational challenges in terms of product mix and distribution that impact its profitability, though it is looking at corrective actions to increase the share of non-par products and sell policies via partners like Policybazaar.

THE FUTURE TRIGGERS

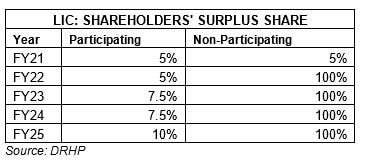

LIC has some things going for it now with the changes in its surplus distribution policies. Till recently, LIC had just one life fund from which it distributed the surplus to policyholders and shareholders in a 95:5 ratio. That’s changed. The life fund has been split into a participating fund and a non-participating fund and from now on, 100 percent of the non-participating surplus will be allocated to shareholders and their 5 percent share in the participating fund will rise in steps to 10 percent by fiscal 2025.

What this means is that there is an incentive from a profit point of view for LIC to focus more on non-par products (as 100 percent surplus goes to shareholders), and its profit margins will further improve by fiscal 2025, with a higher share of participating surplus. To give you a sense, on a steady state basis the current value of new business margin (indicator of profitability for insurers) will improve to 12.3 percent from 9.9 percent with the change in the surplus distribution policy.

According to Credit Suisse, a 10 percent shift from par to non-par can push up value of new business (VNB) margin to 20 percent and raise absolute VNB to Rs 8,500 crore for fiscal 2021, up from the post surplus adjustment VNB of Rs 5,199 crore. That is a significant leap.

Can LIC manage such a big shift? That remains the important question. Competition is bound to spread the word that its policies would become less attractive given the new surplus distribution policy. This more so for non-par products, but even for participating products that are its mainstay. LIC itself admits: “The changes in our Corporation’s surplus distribution policy may reduce the attractiveness of our participating products, which could have an adverse effect on our business, financial condition, results of operations and cash flows”.

So, while there remains a promise of better profitability ahead, how much better remains a matter of judgement. The pricing of the IPO will hence remain key to the response of investors. And here, the government has its task cut out to balance the political implications of selling cheap vis-à-vis offering an attractive price to draw in more investors.

.jpeg)

0 Comments